Cosenza (Italy), 17 Febbraio 2011

Premessa

Proprio ieri, mentre ero alla ricerca di dati sul tasso di cambio Dollaro USA/Yuan cinese, sono capitato su un sito di informazione cinese e vi ho trovato il seguente articolo 16/2 "

'Naked officials' must bare it all about families", a cui non ho dato molta importanza, se non la legittima curiosità di una notizia proveniente da molto lontano.

Nell'articolo si dice che le autorità cinesi hanno annunciato provvedimenti molto severi contro i pubblici ufficiali e i loro familiari residenti all'estero (c.d. "naked officials" o "funzionari nudi"), che ricevono dividendi da società straniere, sono titolari di attività commerciali all'estero, o che si fanno corrompere accettando denaro.

Vedi: "Naked officials are believed to have a greater tendency toward corruption because the presence of their spouses overseas makes it convenient for them to funnel bribe money and other ill-gotten gains out of the reach of local authorities. If caught in their misdeeds, such officials also have an easy means of escape: they simply take up residence with their spouses abroad. (...) In recent years, reports have grown increasingly common of corrupt Chinese officeholders and their families fleeing the country after amassing huge amounts of money. Many naked officials are believed to have sought shelter in rich countries that do not have extradition treaties with China".

La mia prima impressione è stata che si tratta dell'ennesimo giro di vite per impedire che valuta cinese venga investita all'estero...ma oggi ho capito il perchè!

Resoconto

In particolare, all'iniziale limitato mercato di compravendita di Yuan cinesi sul territorio di Hong Kong (soprannominato "dim sum bonds"), se ne sia presto sostituito un altro molto più sofisticato, conosciuto come "synthetic yuan bonds" cioè titoli obbligazionari denominati in Yuan cinesi ma contrattati in Dollari USA.

In pratica, investitori pagano in Dollari per acquistare questi bond, che a scadenza restituiranno capitale più interessi in Yuan cinesi.

Il vantaggio di questo tipo di investimenti si spiega in presenza di aspettative di apprezzamento dello Yuan, cioè se a scadenza il valore dello Yuan sarà maggiore del loro valore corrente. Non solo, ma anche la facilità

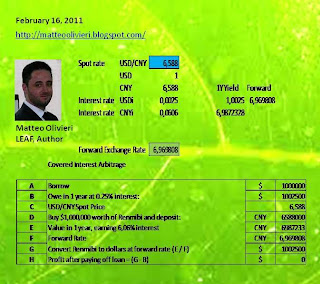

Dopo aver letto la notizia e rintracciato i dati di mio interesse che mi permettessero di avere una stima del tasso di cambio forward sullo Yuan cinese (come si sa, il mercato dei titoli derivati in valuta in Cina è di fatto inesistente visto che la Banca Centrale attua un tasso di cambio fisso nei confronti del Dollaro USA), ho ottenuto i seguenti dati (vedi tabella qui sotto):

In pratica, da una mia stima del tasso di cambio a termine dello yuan (renmibi) cinese, questo dovrebbe essere circa pari a 6.969808, ben al di sopra del tasso di cambio corrente del 6.588 (dati del 16 Febbraio 2011). In altre parole, se i miei calcoli sono esatti, ciò vorrebbe dire che i mercati finanziari internazionali prevedono un forte deprezzamento della valuta cinese nel futuro, ma per il momento conviene scommettere contro lo Yuan qualsiasi cosa accada al tasso di cambio fissato politicamente. Infatti, sia un apprezzamento dello Yuan rispetto al valore di 6.588, sia un deprezzamento fino (!) al valore di 6.969808 consente di ottenere dei profitti!

Questo vuol dire che, prendendo a prestito in Dollari USA e depositandoli per un anno su un conto bancario ai tassi di interesse correnti USA, e poi convertirli in Yuan cinesi ai tassi di interesse correnti cinesi e al tasso di interesse a termine, si può ottenere un profitto per ogni tasso di cambio inferiore a 6.969808. Per tassi di cambio superiori a 6.969808 si incorre in perdite.

Così si spiega sia perchè le autorità cinesi sono tanto allarmate dagli "speculatori internazionali", sia perchè gli intermediari finanziari di tutto il mondo si stiano lanciando in questa nuova avventura di scommesse contro la valuta cinese.

L'unica difficoltà potrebbe essere data dal trovare il modo per far rientrare in Cina questi capitali una volta riconvertiti in Yuan...ma sono sicuro che il mercato troverà il modo per aggirare questi ostacoli politici.

Per chi fosse interessato a maggiori dettagli su rischi e opportunità derivanti da questa forma di investimenti, ecco un lungo stralcio dell'articolo Reuters citato sopra:

"Synthetic bonds are riding on the wave of investors migrating their assets from U.S. dollars to renminbi," said a banker who worked on Evergrande Real Estate Group's jumbo 9.25 billion yuan ($1.41 billion) synthetic deal that priced last week. Evergrande's two-tranche issuance was the biggest high-yield bond deal ever in Asia. "The beauty of the deal is that the investors do not need to have any renminbi funding. (...) Last year only saw one synthetic deal come to market worth 3 billion yuan, while the burgeoning dim sum bond market produced 33 deals worth about 42.6 billion yuan. Twenty days into 2011 and there were already 15.8 billion yuan of synthetic bonds issued and 4.5 billion yuan of dim sum debt. Most of the yuan outside of China is collecting in Hong Kong, which has become the laboratory for Beijing's attempts to spread the use of its currency abroad. At its current rate of growth the yuan deposit base in Hong Kong could hit 2 trillion yuan this year from 280 billion yuan as of November 2010. (...) Last year high-profile multinational companies like McDonald's Corp and Caterpillar Inc tapped Hong Kong's yuan market, also called the CNH market, for symbolic amounts of funding, but the bureaucratic process of moving the money into China is daunting for many borrowers.

Ironically, yuan raised in Hong Kong is treated like a foreign currency by China's foreign exchange regulator. The speed that it takes to get the "foreign yuan" into China depends on the location of the borrowing company's mainland operations, because provincial governments ultimately handle the process. By contrast, the average time that it will probably take to get dollars raised via a synthetic bond into the mainland is around four weeks, including the time taken for preparing documentation, debt bankers said. For a repeat issuer, like Shui On Land, which has issued two synthetic yuan bonds in a month, it could take around two to three weeks, they said. "CNH remittance is approved on a case-by-case basis. There are no clear existing guidelines on this. But the procedures are well in place for USD inflows into China. There is a clear channel where you go through the necessary steps," Vivian Wai-man Lam,partner with law firm Paul, Hastings, Janofsky & Walker in Hong Kong, said. Lam advised China SCE Property Holdings on its 5-year, 2 billion yuan synthetic deal that priced on January 7. Unless Beijing makes its capital account more porous in the near term, she expects high-yield borrowers in the offshore yuan market to choose synthetic rather than dim sum bonds, especially since the funds are cheaper than the dollar bond market. Nomura said in a research note Evergrande's synthetic 5-year paper that priced at 9.25 percent would have had an equivalent yield of about 11.8 percent if the company did a straight U.S. dollar bond without the renminbi exposure. For investors, the synthetic bonds are not without their risks. Evergrande's 3-year and 5-year bonds dropped to 99.25 almost immediately in the secondary market after pricing at par, despite meeting overwhelming demand in the primary market. Some bankers said that this was because investors ended up with more bonds than they wanted because the competitive order book made them over bid. Another risk is sector concentration. All four issuers of synthetic yuan bonds in the past month have been Chinese property developers. Investors may at some point think twice about the risks surrounding an industry so vulnerable to further policy tightening in China and demand higher yields. For now expectations of yuan appreciation is clearly outweighing any of the risks associated with yuan assets. The yuan has risen more than 3 percent against the dollar since June when China announced it was loosening its grip on the currency. Though it is still tightly controlled, a Reuters poll earlier this month showed economists see the currency rising a further 5.4 percent over the next 12 months as Beijing tries to quell inflation. "If investors maintain the view of an appreciating Chinese currency, they will continue to accept a lower yield in return for exposure to an expected rise in value for the RMB, thus making synthetic RMB bonds relatively attractive vis-à-vis U.S. dollar ones for Chinese issuers," analysts from Moody's Investors Service said in a report on Wednesday. Indeed, at a time when mainland money markets are increasingly volatile and Chinese bond yields are surging on expectations of tightening policy, offshore yuan capital markets are booming. "Borrowers are filling their boots while they can," said the head of debt capital markets at a bank in Hong Kong".

AGGIORNAMENTI

Lunedi 21 Febbraio 2011: Ecco un altro tassello a sostegno delle mie tesi: nell'articolo CNBC 18/2 "

An Optimist On The Yuan Has Little Yen For The Yen", una delle più grandi banche del mondo scommette su un apprezzamento della valuta cinese del 4,5% quest'anno!

Vedi: "Credit Agricole's head of global FX strategy expects the yuan to appreciate 4.5% this year, but the yen to move lower. Mitul Kotecha told CNBC that China is unlikely to respond to pressure from G20 members on its currency, but it will still let the yuan rise gradually in the face of all that economic growth".

Martedi 22 Febbraio 2011: Ecco tre grafici che mi sembrano riassumano tutta la "drammaticità" del problema (Fonte

FAZ): in un contesto certamente inflazionistico, si tenta in tutti i modi di risparmiare per frenare la crescita dei prezzi.

Nel primo grafico si vede il livello aggiornato dell'inflazione cinese, per singoli settori dell'economia (cibo, assistenza medica, alloggi, ecc.).

Nel secondo si vede una stima del tasso di ambio effettivo cinese. In particolare, la differenza tra il valore reale ed il valore nominale, è un indice dei risparmi generati per combattere l'inflazione domestica.

Nel terzo grafico si vede come i risparmi in generale derivino da minori crediti concessi dal settore bancario e da aumenti delle riserve minime bancarie (scala destra invertita).

Matteo Olivieri

>> Le informazioni qui contenute non (!) costituiscono sollecitazioni ad investire.